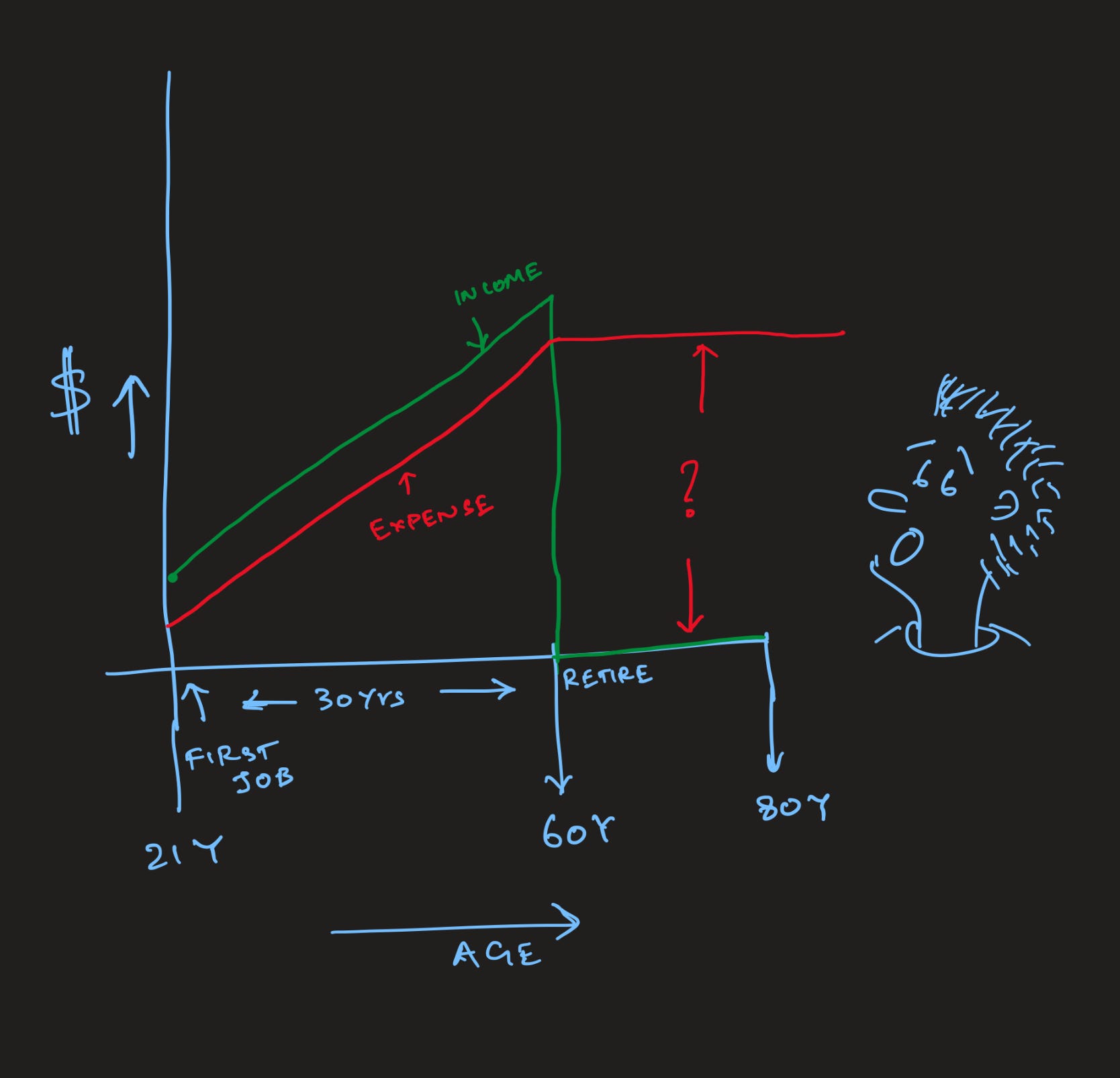

Lifestyle inflation is defined as “an increase in individual’s spending when an individual's income goes up”. If you are in your thirties or above, there is a chance that you can relate to this more. When I first got my job my salary was Rs.16000 - my expenditure included rent and electricity (shared with two other guys), dinner (not fancy) and internet. Now, 15 years later - I pay for OTT, rent and utilities, car fuel, kid’s school fees, cook… etc. In your case, maybe today, 16000 doesn’t even cover your rent. This is what lifestyle inflation looks like. As my salary grew, my expenses also grew by choice (not by chance). If you are not careful about this increasing expense, it could lead to problems in the long term.

Lifestyle inflation looks different for different people and most of the times we will have a reason to justify these expenses. Everything is hunky dory when there is constant stream of income, the real problem occurs in the long term:

Your savings will get affected. If you are earning 50,000 and you are spending 45,000 then you are saving only 10% of your income. And if you continue down this path your corpus for your retirement is going to be very less. The problem only worsens when it becomes hard to get rid of the luxuries that has become part of life - cook, driver, car(s), OTT subscriptions, rent (or maintanance of a big house) etc.

The way to avoid it is to save first and the spend the remaining. There are retirement calculators available (I made one too) on the internet. Saving 40% of the income seems to be a good benchmark and investing that money wisely can help with a more comfortable retirement.